Owning the rails

The internet finance thesis is right on track

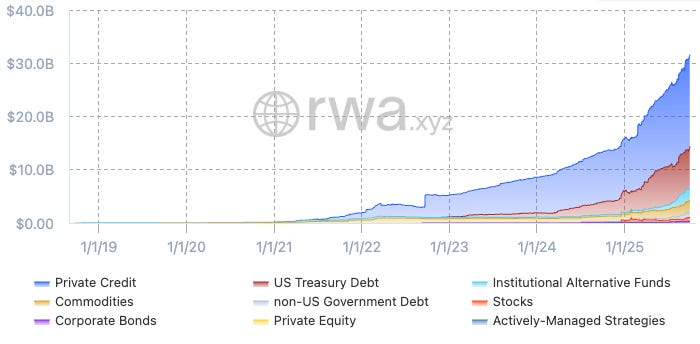

Last quarter, we wrote that crypto was ‘crossing the chasm’. With a favorable regulatory environment in place, stablecoins are leading the way towards mainstream adoption. More assets are being tokenized, more use cases are emerging, and more companies are building. Stablecoin supply is approaching our year-end target of $300B and still makes up the majority of “real-world” assets on chain – but issuance elsewhere is inflecting too.

Predictions that once seemed fantastic are now showing up in the data. As finance and crypto converge, there will be huge outcomes for those that own the rails and infrastructure. One interesting wrinkle this cycle is that it’s less obvious those winners will be crypto-native. Stripe’s recent launch of its own blockchain illustrates that point. It’s validation for the space but also a shift away from token networks to embedded finance platforms. That’s both inevitable and healthy — a sign that crypto is becoming part of the financial substrate rather than an alternative to it. But it’s also a departure from the cypher punk ethos and previous value accrual models.

Volatility down, dispersion up

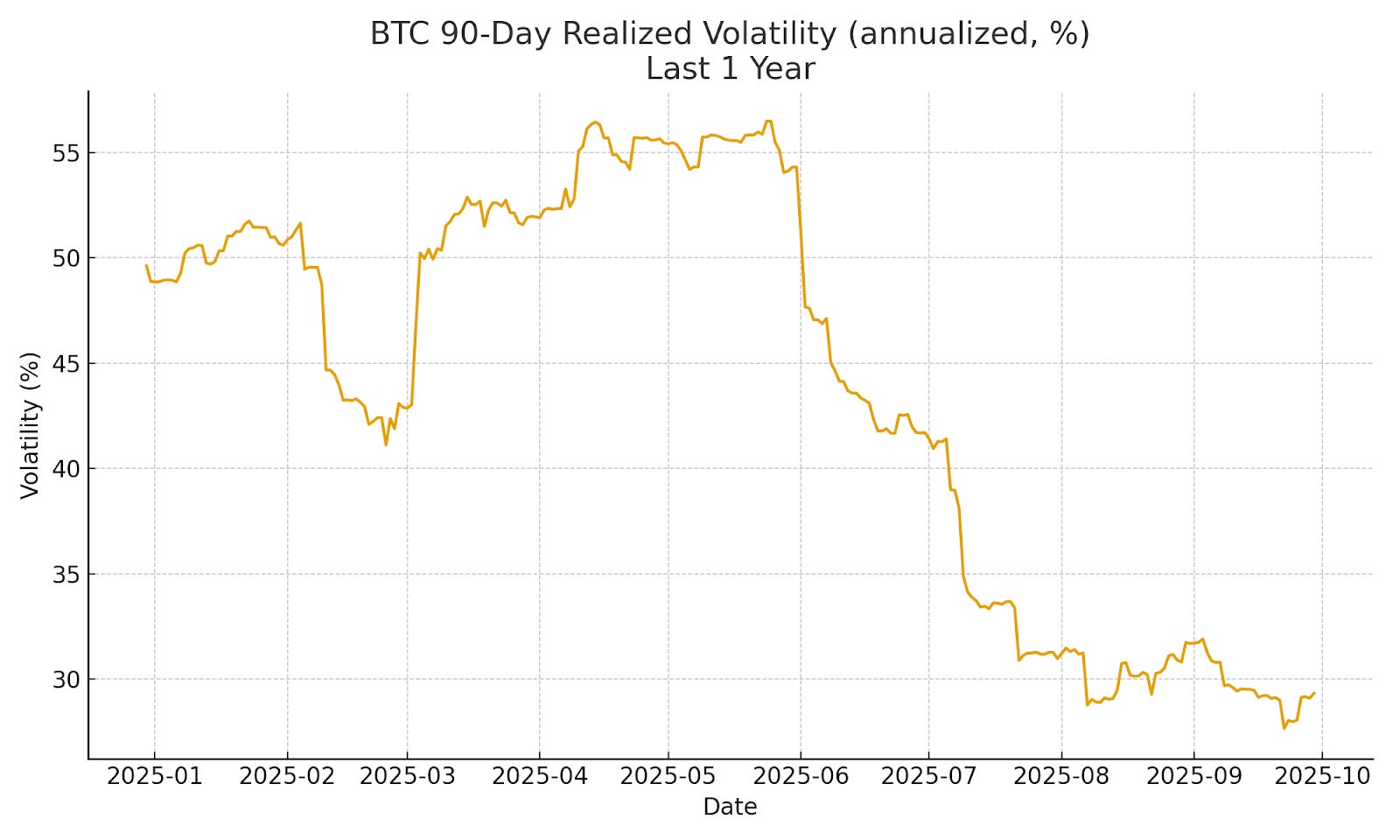

So what does that mean for crypto markets? We think it means that valuable financial apps and infrastructure will continue to separate from other projects with less obvious PMF. Crypto investors have come to expect two things: high volatility and low dispersion. Crypto is obviously still volatile, but the major assets in the space are markedly less volatile than they used to be. This is largely a function of institutional ETF flows providing consistent price support, as well as evidence that Bitcoin is becoming a more mature asset.

At the same time, dispersion between assets is higher than ever. Jeff Dorman pointed out that 75% of the market is down YTD, with most down 40% or more. That is quite unusual for what we would consider a bull market, and further underscores a point we’ve made before about asset selection. It is entirely reasonable for good tokens to go up while bad tokens go down, and we expect that trend to continue as the marginal buyer becomes more sophisticated. It is now harder to pick winning tokens in liquid markets, but doing so is the only way to outperform BTC.

What we’ve still been buying

The obvious question: What makes a good token? If you’ve read our letters before, you can guess where this is headed. In short, the same things that make a good business. Mostly, a useful product that customers are willing to pay for. Also, and this part is unique to crypto, a mechanism to accrue value from the use of those products to tokenholders. And finally, a reasonable capital structure that aligns stakeholder interests and allows the token to appreciate as business fundamentals improve.

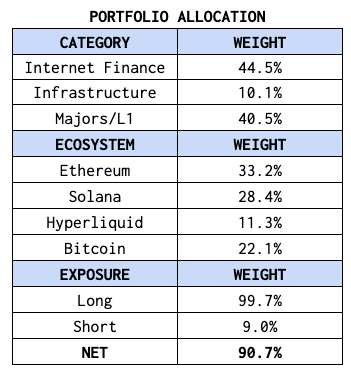

95% of tokens still do not meet this bar. Many things in crypto are not working, and many more tokens are poorly designed. But the one thing that is unequivocally working right now is internet finance and capital markets. Consequently, those now make up nearly half of our portfolio and the majority of non-major holdings. As more assets come on chain, more financial activity will follow, and the applications that facilitate those transactions should benefit.

AAVE continues to dominate lending markets

Among the existing on-chain businesses, lending might be the best. While not as profitable as exchanges, the moats are more durable and the tailwinds are arguably stronger. On-chain banks have structural advantages over incumbents, and they are the most obvious destination for the tidal wave of stablecoins that is coming now that GENIUS paved the way for institutional capital to access them.

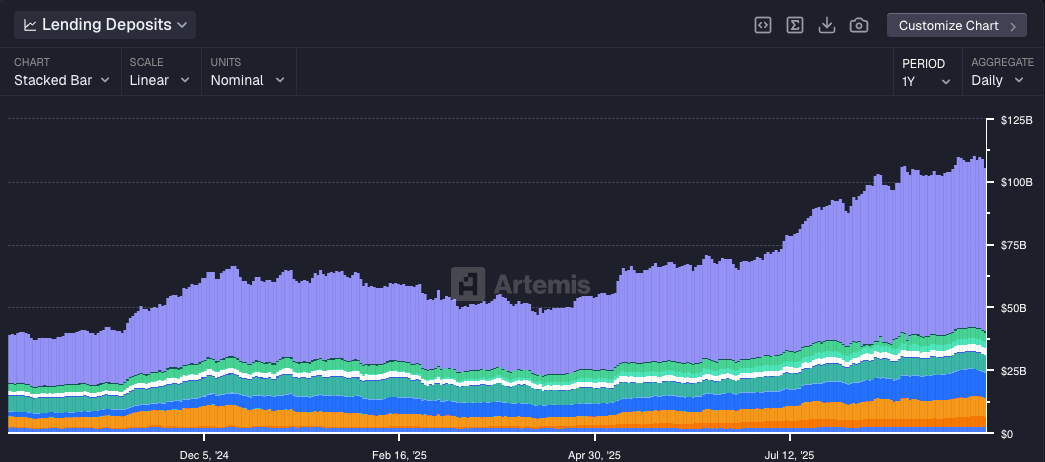

AAVE is the undisputed category leader, accounting for nearly 40% of all TVL on Ethereum. TVL isn’t perfect , but deposits are a good measure of actual demand in the case of lending protocols, and demand for AAVE is strong and getting stronger:

There are two stories here. The first is the secular growth of online lending. That’s limited to on-chain assets like ETH, but in the future will include many more collateral assets. Imagine applying for a home loan without ever talking to anyone at a bank. That is a future companies like Figure (which IPO’d in Q3 for $5b) are building towards.

The second is the increasing dominance of AAVE (purple). Ethereum is attracting new lend and borrow activity, and it is disproportionately happening on AAVE. Despite being an order of magnitude larger, AAVE still grew faster than all of its nearest competitors in Q3.

At ~$70B in deposits, AAVE is now the 36th largest bank in America (and climbing). They are executing well, with a renewed focus on value accrual (via buybacks) and a targeted approach to growth. We appreciated the decision to pull back from failing L2s and push harder on strategic integrations that can actually make a difference. Early efforts on Plasma have done well.

It may not be “cheap” relative to other finance protocols, but we view this as paying for quality. AAVE has a legitimate moat in liquidity and reputation, as well as a strong balance sheet and outstanding leadership and governance.

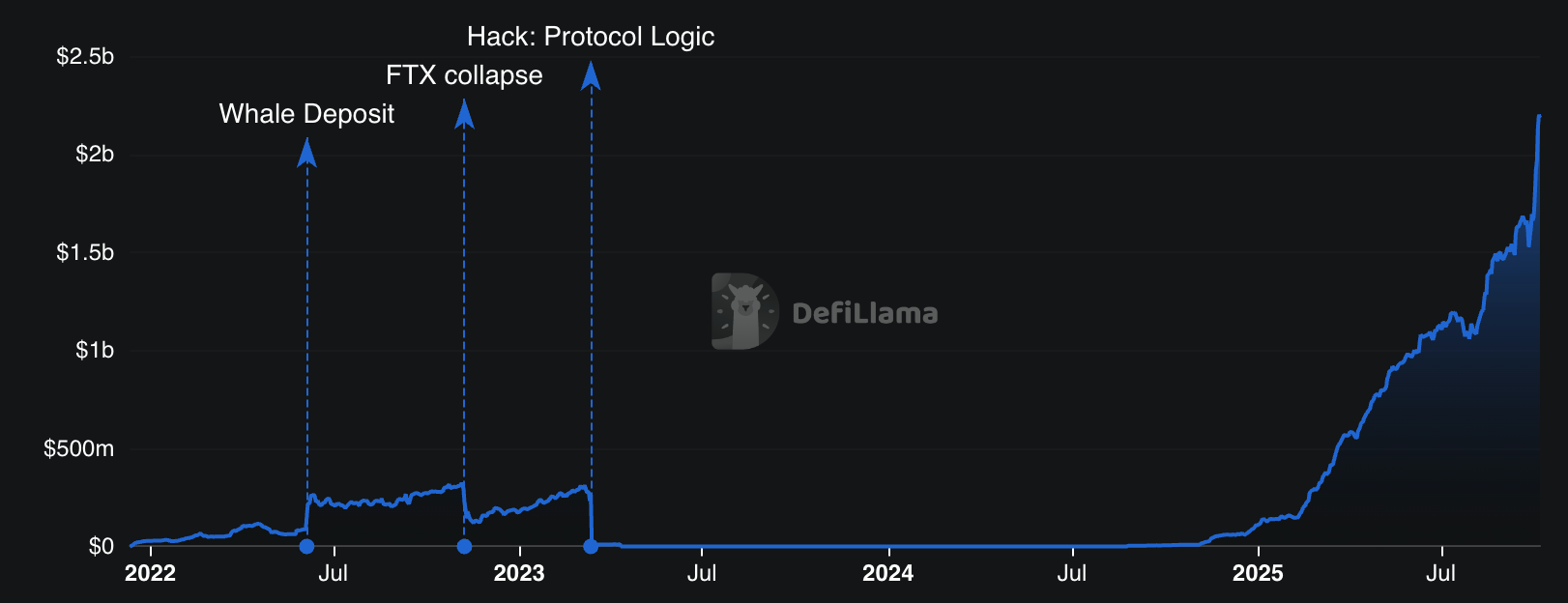

Euler emerging as an innovator in lending

In crypto, sometimes success is a function of survival given the number of landmines. Euler – which focuses on customized lending for longer-tail assets – hit a major landmine in 2023 when a hacker drained $200m from pools in an exploit. The TVL chart shows a protocol left for dead, as you’d expect in an industry where security incidents are hard to forget.

But Euler was not dead. The team scrambled to plug the hole, ultimately recovering all of the stolen funds. More importantly, they kept the team together and improved the product. 2025 bore the fruit of that labor, with TVL surging past $2B on the back of its v2 launch. Some of this was driven by incentives, but the team still deserves most of the credit for the resurgence and remain appropriately focused on profitability.

At a ~$200m valuation, Euler is still undervalued relative to recent growth. Its closest comp, Morpho, trades at 5-10x the valuation despite comparable metrics. Notably, Euler is generating that revenue on a fraction of the TVL, a testament to the capital efficiency of v2. Furthermore, this value already accrues to users through a novel Fee Flow auction mechanism.

We expect BD partnerships to drive an outsized share of growth in this space moving forward, and hope to help the team here now that we have a position. Morpho ran this playbook well with Coinbase, but there are many platforms that could benefit from a partner that can deliver flexible on-chain lending at ultra-competitive rates.

With 10x YoY growth in a sector we believe in, a profitable business that already accrues value to the token, and a team that has demonstrated grit, integrity, and long-term orientation, there’s a lot to like about $EUL.

Ethena out executing everyone for yield on chain

Ethena is a new sort of protocol that doesn’t fit cleanly into the categories of exchange, lending or perps. Technically it is a stablecoin business, but the real product is yield. This yield comes from delta-neutral hedging profits, which are wrapped and distributed to holders automatically. By pairing spot crypto assets with short futures positions, Ethena generates yields which do not depend on US T-Bill rates. That yield has fluctuated between 4% and 12% this year, and moves in line with demand to borrow in crypto markets. In a declining rate environment, this should become more attractive to investors seeking low-risk, dollar-denominated yield.

Supply is up 6x YoY to $15b, making it the third largest digital dollar behind USDC and Tether. Given the premiums both trade at, the valuation upside is clear if Ethena continues to grow. Holding ENA is definitely a bet on their stablecoin business, but it’s also a bet on the team to seek yield and expand distribution elsewhere on-chain. This is evident in their recent expansion into the Hyperliquid, Binance and Sui ecosystems with native products. Founder Guy Young is widely regarded as one of the few best entrepreneurs in the space and the team is operating at a relentless pace.

Hyperliquid enters the stablecoin wars with a bang

Most people assume stablecoin issuance is an amazing business because Tether is an amazing business. But most stablecoin businesses are actually not that great. They can’t clip 4% forever without passing any of it back to retail holders (less if rates decline). They have to cut deals with distribution partners such as Coinbase to grow, which results in them paying 50+% of revenue in exchange.

What is actually an amazing business is Hyperliquid, as evidenced by the number of attractive partnership offers it received to issue its native stablecoin. We preferred the losing proposal from Paxos to the winning proposal from Native Markets, but this is still a great outcome for the ecosystem. Most of these teams will stick around (e.g. Ethena) and offer products that are both novel and useful, such as holding collateral for hyperliquid in USDe, which can earn 10+%.

Hyperliquid has plenty of competition now from Aster, Lighter, and others, but we are still betting on this team and community to define the frontier of on-chain trading. There will be plenty of TAM to go around as the rest of the world realizes that perps are a superior way to trade derivatives (vs. options) and more assets begin to trade (e.g. public equities).

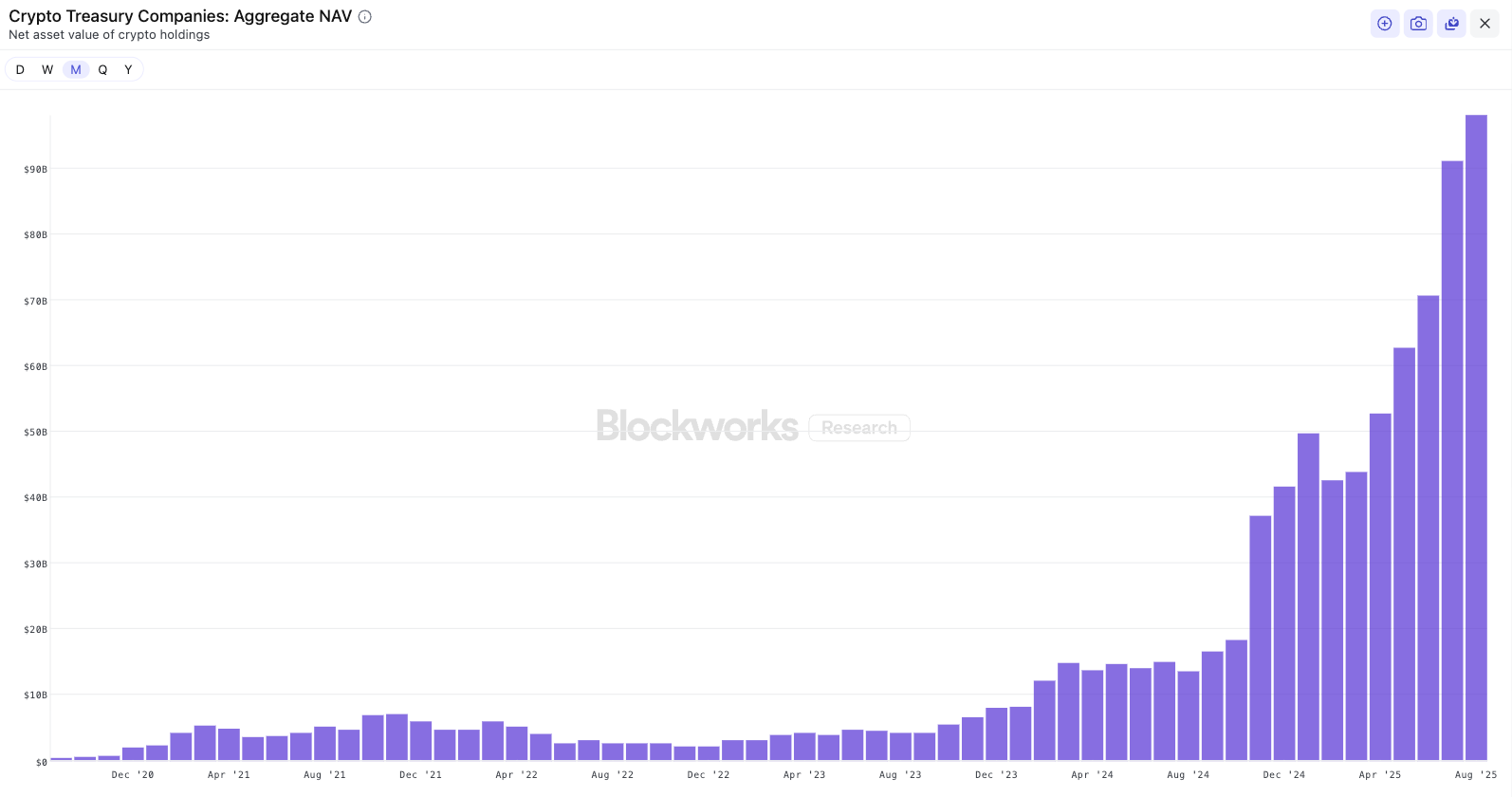

Digital Asset Treasury Companies boom, for now

The other big story in crypto this quarter was digital asset treasury companies (DATs). Michael Saylor’s Bitcoin DAT (Strategy) has been so successful that dozens of copycats have now emerged to replicate the model for other assets. DATs promise a retail-friendly vehicle that will increase tokens per share over time, but in reality, they look more like zero-sum financial engineering. The idea of generating yield through staking and on-chain activity is good in theory, but the capital structure for most of these companies is overly favorable to sponsors and insiders. This has some appeal for equity-only investors that want exposure to crypto (and traders), but the underlying mechanics (and potential for downward reflexivity) make them basically untouchable for long-term holders.

With that said, they have been quite successful at attracting capital. Across all assets, DATs now hold almost $100B, and the flows from the big Ethereum DATs (Tom Lee’s $BMNR, Joe Lubin’s $SBET) pushed Ethereum towards an ATH in Q3. We don’t dismiss their market impact – SOL is set to potentially benefit in Q4 – but DATs are not a good use of time or capital for most investors.

Outlook and positioning

While we see some signs of froth (DATs being the most high-profile example), we won’t be joining many in crypto in calling for a 4-year cycle top. We are still looking for opportunistic short exposure to overbought tokens, but the broader macro setup and regulatory tailwinds are simply too strong to fade at this point.

From a macro perspective, crypto held up well during a Q3 marked by seasonal softness and mixed indicators. Liquidity tightened as expected with the TGA requiring replenishment, but the mandate is growth and spending will continue. The biggest headlines were around the Fed, which continues to balance its dual mandate in an increasingly fraught setup. Backward revisions to employment data revealed a weaker labor market than expected, effectively forcing the Fed into a rate cutting cycle despite the fact that asset prices are at all time highs. This is unusual, but still suggests a supportive environment for risk assets. The amount of cash in money market funds is also at all time highs, and those dollars need to go somewhere if rates decline.

Additionally, the growing influence of the President and Treasury over the Federal Reserve signals the emergence of a stronger “Fed put” into 2026. With Chairman Powell’s term ending next spring, Trump’s likely appointees will prioritize growth (e.g. stimulus checks) in hopes of outrunning the debt. Setting aside the broader impacts of an emerging two-tier economy (those who own assets and those who don’t), this is a favorable setup for high-quality risk assets in particular.

The other reason to stay long crypto is regulatory. This year marked a turning point for crypto policy with two landmark legislative proposals, and we are just beginning to see the impact. The GENIUS Act was signed into law in July, effectively legalizing stablecoins and setting off a flurry of deals as incumbents scrambled to catch up. Just about every major bank and fintech player is now actively considering some form of issuance or partnership, if not their own blockchain (e.g. Stripe’s). Not all of them will succeed, but the upside is simply too large to ignore (case in point: Tether recently announced a capital raise at a $500B valuation).

The second piece of legislation, the Clarity Act, aims to establish a comprehensive regulatory framework for digital assets by defining parameters and instantiating regulators. It’s uncertain if Clarity will pass this year, but when it does, we expect a surge in interest in altcoin investing akin to the stablecoin boom we’re seeing right now. Despite improving fundamentals, altcoins still remain below the line for most institutional investors. But with the regulatory overhang cleared and more attention on the underlying assets, the market should reward assets that deserve to be re-rated.

We continue to rotate out of majors and into high-quality alts in anticipation of this dynamic, and are risk-on going into Q4.