Crossing the chasm

Towards a more on-chain future

Q2 was quite the contrast to Q1, with markets snapping back to pre “Liberation Day” levels as tariff fears diminished and Trump relented on fiscal austerity. There are still risks in a Trump economy, but it’s clear that the mandate is growth. This growth-first outlook has coincided with increasingly ambitious crypto plans from Fortune 100 companies as a favorable regulatory landscape in America takes shape. We think history will view this year as a “crossing the chasm” moment for crypto akin to 2004 for the web – after the dot com bubble had cleared, when Facebook was founded, and Google IPO’d (and launched GMail). Similarly, crypto is both growing up and still in its early days, with institutional interest in Bitcoin and stablecoins leading the way toward mainstream adoption.

Bitcoin dominance marches higher

Bitcoin ETFs continue to break records with Blackrock’s $IBIT reaching $70B AUM in less than a year. For reference, that is 5x faster than the biggest gold ETF ($GLD), and Bitcoin ETFs have already surpassed gold ETFs in daily flows and will soon eclipse in AUM. The list of holders includes many of the biggest funds globally (Brevan Howard, Millennium, Mubadala, and Citadel are all in the top 10). This has led to YTD outperformance of BTC (+15%) while other majors are down 20% and some alts are down 30% or more. The trend towards dispersion continues, underscoring the importance of active management and asset selection beyond BTC, which is trending back towards ATH dominance at 65% ($2.2T of $3.4T total crypto market cap).

Stablecoins lead renaissance in “Internet Capital Markets”

The most notable stamp of approval came from the US Senate with the passage of the GENIUS Act in mid-June, which was the first bi-partisan piece of legislation this session and will effectively legalize stablecoins once it passes the House. As we’ve said before, stablecoins are a boon to American dollar dominance and an increasingly important payment and savings instrument globally. It’s encouraging to see Congress recognize that and create a framework that enables further adoption on-shore. The language leaves a bit to be desired in terms of design space, but is a huge step forward that will bring many more US firms onto crypto rails in the coming quarters.

You will sometimes hear critics dismiss stablecoins as a crypto use case because they don’t fit the expectation of an alternative currency. But that is in fact their appeal, since most people choose to denominate in dollars. Stablecoins offer the best of both worlds – an upgraded product in what is already the world’s most preferred and liquid market. In January, we predicted that the supply of stablecoins would grow by 50% this year from $200B to $300B. At the halfway point, we are right on track with supply nearing $250B, and a small but growing long tail of upstarts.

Tether still dominates, but USDC (Circle) won the PR battle this quarter with its mega-successful IPO. We don’t foresee anyone dethroning Tether globally for now, but with regulatory approval in the US, many players will compete for domestic growth by issuing stablecoins targeted at their existing user bases. JP Morgan, Amazon, Walmart and Uber all announced such initiatives in Q2. We are most interested in products that combine the form factor of tokenized dollars with built-in access to on-chain yield or other holder benefits (e.g. a higher savings deposit rate for JPMD, discount for purchasing with AmazonUSD).

Stripe deserves a lot of credit for bringing this opportunity to market. First was their $1B acquisition of Bridge, the leading provider of b2b stablecoin infrastructure. Their more recent acquisition of Privy (an embedded wallet provider) shows that they want to own a full-stack solution to offer merchants the benefits of stablecoins without asking them to change their existing workflows. Now, via partnership with Shopify, merchants can process USDC transactions globally at a potential 60-80% cost savings vs existing payment processors. Few in tech are more respected than Stripe and the Collison brothers, and they are all in.

As for what’s ahead, it’s hard to overstate the size of the opportunity. But don’t take it from us. The US treasury published a comprehensive report that projects $2 trillion of on-chain stablecoin supply by 2028 (a 10x from here). They have since updated that number to $3.7T after the passage of the GENIUS Act. A tidal wave of stablecoins are coming in the next few years whether you like them or not.

But while stablecoins may be the biggest narrative in crypto, they are hardly the most investable. At this point, Circle equity is wildly overbought and there are few other ways to get direct exposure to stablecoin growth. But with this influx of internet capital liquidity, the obvious beneficiary will be internet capital markets and the protocols that facilitate lending, borrowing and trading of internet dollars.

Outperformers in ‘Internet Finance’

If you assume that new stablecoins largely flow into existing protocols, winners can realistically expect to 10x their current users, volumes and earnings over the next several years. In the past, we might have expected a rising tide to lift all boats in the alt coin market. However, as we wrote last quarter, this is a new market regime:

So is this time really different? That’s a dangerous assumption to make, and we do still expect individual alt coins to outperform majors when risk appetite returns. But we do not expect altcoins to outperform in a highly correlated way as they have in the past. Rather, we expect isolated outperformance based on actual business and revenue growth, not cycle timing and narrative favor.

What we’ve seen this quarter is exactly that, as projects with fundamental traction and value accrual have led the market. We’ll highlight the three most relevant.

Let the $SYRUP flow

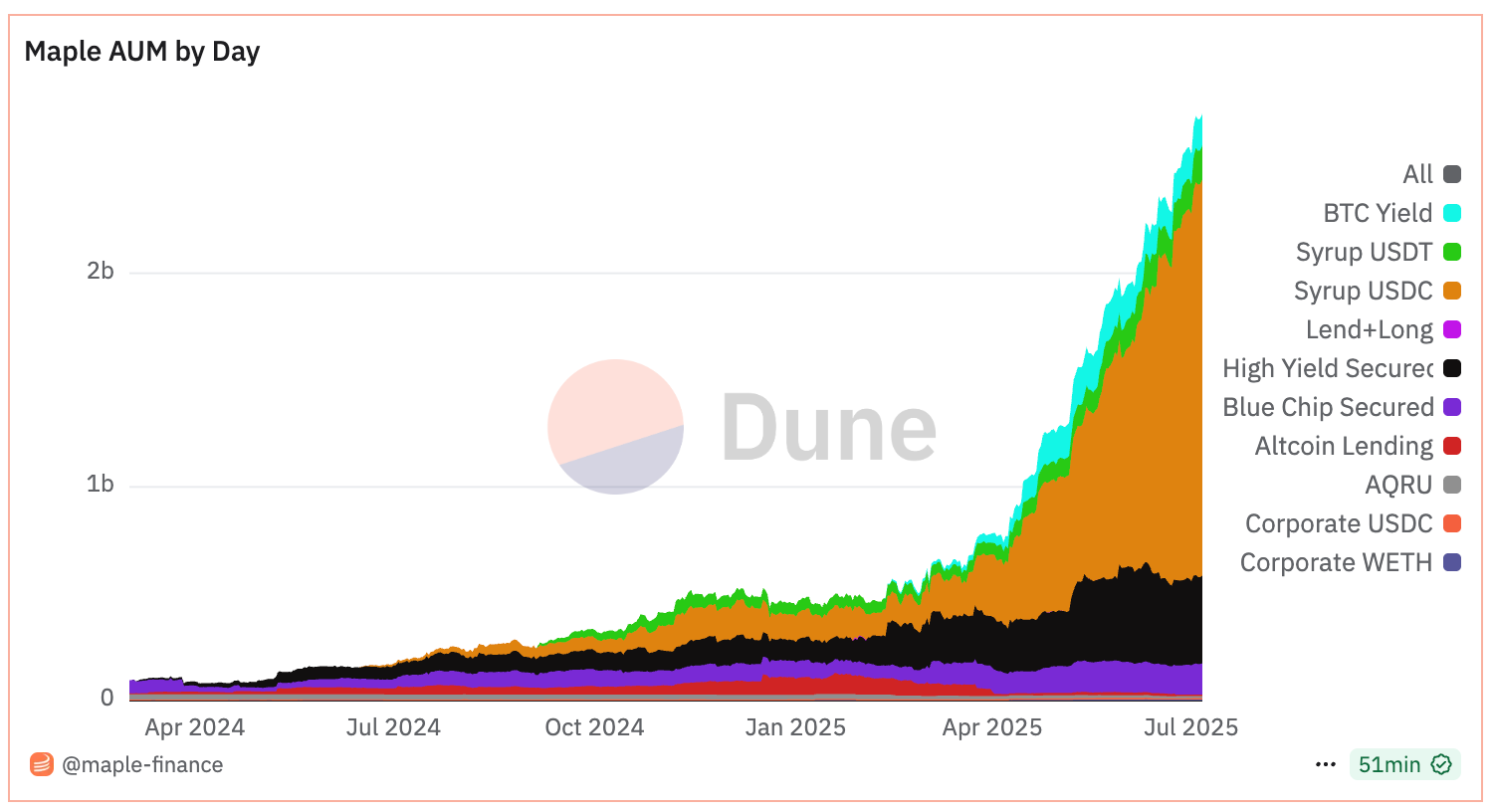

The best example of this is Maple Finance (formerly $MPL, now $SYRUP), whose AUM chart is one of the best you will find:

Revenue growth has tracked AUM (now at $1.3M MRR), leading to a 5x increase in token price since April 1. Maple is a deserving internet finance darling, having been left for dead in a brutal bear market but now an emerging category leader with a committed team that continues to ship compelling new credit products. A Binance listing and multiple savvy distribution partnerships with other protocols have also helped.

Maple has grown into a core position for us despite taking some profit in Q2.

The $HYPE is real

We called out Hyperliquid in our last report as an interesting and fairly valued growth story, which further accelerated in Q2. Hyperliquid is now the most profitable protocol in crypto with nearly $800M in annualized revenues. They have already eaten much of the on-chain perps market and are now starting to seriously threaten CEX incumbents like Binance.

Hyperliquid is a good example of not needing to move first to win a category. DYDX and GMX both had headstarts, but were badly out executed on product, go-to-market, and tokenomics. The success of the native token, $HYPE, is a case study in and of itself. 97% of protocol fees are used to repurchase HYPE tokens, implying a ~7% buyback yield that is on par with the most aggressive share repurchase programs in trad markets. But what makes Hyperliquid unique is that they’re also growing 8x YoY.

At current market cap it’s no longer cheap, but there is considerable momentum around its L1 and developer platform. Competition in the perps market will remain intense (Coinbase and Robinhood are coming), but we would still bet on Hyperliquid to own the permissionless niche and leverage its tech and community to offer novel infrastructure that grows the business. HIP-2 and HIP-3 are good examples of this, and have already resulted in at least one market-expanding partnership with Phantom. We were buyers of HYPE in early Q2 and it has grown into a core position.

Maker becomes $SKY

No one can match Hyperliquid for on-chain earnings, but Sky is still highly profitable (~$100m in annual earnings) at a fraction of the valuation. We’ve written about it plenty, but a few notable things occurred in Q2:

Token transition from MKR to SKY, which will likely result in 15-20% decay to token supply (as a result of old coins that don’t migrate to the new contract)

Launch of staking rewards (i.e. dividend yield) which currently pays 13% in USDS (their native stablecoin)

Re-launch of buyback program, which is on pace for 10% annualized buyback yield

The Sky rebrand was messy at best, but at this point the roadmap is more focused and token economics have vastly improved. With SKY, you own a stable and profitable existing business at a good price (sub $2B valuation) in a great sector with huge upside if any of its growth initiatives prove successful in increasing supply of USDS. That is a big if, and plenty of people quibble with project leadership, but either way the existing business provides a margin of safety in this rate environment.

Money market moves

The first place most capital will flow on-chain is into money markets (i.e. lend and borrow), of which AAVE remains the 800 pound gorilla. Their $41B in deposits would make them a top 50 US bank. AAVE doesn’t have the same excitement around it as newer projects, but we value its stability and longevity. The strength of its brand and depth of its liquidity should be valuable in attracting institutional capital. They face increasing competition on EVM from Euler and Morpho, who are more innovative and capital efficient, but lag in deposits by an order of magnitude. We view distribution as the big question moving forward with everyone racing to capture new users via partnerships with platforms such as Coinbase (whose deal with Morpho has largely fueled the latter’s rise)

Kamino dominates money markets on Solana and is aggressively expanding into adjacent products such as yield vaults, swaps and perps. They are uniquely positioned to grow with Solana and have launched a number of savvy distribution partnerships with Maple, Marinade and others. It is fairly cheap relative to its peers, likely a function of an aggressive H1 unlock schedule, but is entering the strike zone here if you believe Solana has another leg of growth to come outside of meme coin trading.

The ‘short list’

Although we are obviously long the industry, the sustained underperformance of alt coins over the past several quarters has forced us to re-evaluate certain assumptions. One is that shorting in crypto is never a good idea, because assets are highly correlated and prone to violent rallies. Without dispersion, there is little incentive to short outside of directional exposure or hedging. But that’s not how the market moves anymore, and alt coins with poor underlying fundamentals have fallen hardest in recent sell-offs.

Even at these levels, many coins are still grossly overvalued with multi-billion dollar valuations attached to projects with no real path to revenue growth. We don’t expect speculative fervor to go away or legacy premiums to erode entirely, but market structure has offered an opportunity to bet against tokens that are not worth holding.

We are most interested in betting against two particular types of projects:

Projects with big VC holders and little product market fit: Given how high valuations became, many investors are still vesting tokens in profit that they have to sell to generate returns, price action be damned. With more unlocks ($1.4B per month and growing) than investable capital (liquid funds have ~$10B and 2025 was a down year for fundraising), there are simply not enough buyers for most of these tokens.

Projects lacking value accrual: If you believe the market will reward projects that are attached to good businesses, it follows that it will punish those attached to bad businesses (or in some cases, no business at all). This is a more dangerous game as we’ve seen with memes, but as marginal buyers become more sophisticated, we expect unserious tokens to fade in relevance and serious tokens to be judged more rigorously.

In other words, long quality and growth; short speculative and stagflationary. A few that fit the bill:

Trump ($TRUMP) is among the least serious tokens around with no meaningful value accrual and a ghastly unlock schedule. Over the next 24 months, nearly 800 million new tokens will hit the market, representing $7B of sell pressure at today’s price. It has dropped precipitously since peaking just after launch, but jumped 50% on news in April that top holders would be invited to a private dinner with President Trump. Some viewed the event as an indicator the Trumps will find ways to add value for token holders, but we viewed it as a ham-handed attempt to pump price before unlocks (and an opportunity for us to open a short position). That view was validated when holders reported bad food, lame attendance, and an early exit by Trump, not to mention a 15% sell-off. With pressure mounting on Trump to distance himself from this blatant conflict of interest, there are few if any catalysts to come.

Cardano ($ADA) has a huge market cap ($28B) and not much else. For a brief moment, Cardano was rumored to be included in a potential government stockpile, causing price to double before quickly retracing. It never made any sense for Cardano to be involved (there is little to no momentum), and soon it became clear ADA wouldn’t be. Perhaps the most compelling use case for the token comes from founder Charles Hoskinson, who suggested swapping it for BTC, which could be a good move for the project but won’t help token price.

Optimism ($OP) is an example of a good project with a bad token. Gas on Optimism is paid in ETH and what little fee revenue it does generate does not flow to tokenholders. The only reason to hold it is to participate in governance, which is also becoming less interesting as Arbitrum has turned the tide in the Ethereum scaling wars by luring Robinhood and Ethena to its tech stack recently. Most of OP supply is still held by early investors or promised for future ecosystem use (i.e. emissions).

Ondo ($ONDO) has done quite well as the “real-world asset” narrative gained momentum, and Ondo recently announced it was launching its own chain. We fail to see what value this chain adds, and are skeptical that headlines will translate to users and activity. At a $8B valuation, there is plenty of room to fall as tokens unlock and momentum fades. On a fundamental basis, Ondo looks a lot more like projects that trade at sub billion dollar valuations (e.g. Maple), which are also growing faster.

These are small in size for now, but we expect to add to them if markets rally. In addition to a fundamental bet, it’s also a capital-efficient way to de-risk (especially when longs pay shorts).

Towards a more on-chain future

As we and others have said, the term “defi” is increasingly outdated. Decentralization is no longer a defining characteristic or prerequisite for success. Users don’t need to self-custody tokens in a wallet for crypto to win. Sure users still can, but most will just access crypto products through platforms they already use such as Fidelity or Robinhood, which can embed them inside an already slick UX. The shift to mainstream adoption demands complete solutions, not frontier features. Increasingly, finance will simply be powered by crypto.

This also suggests that distribution partnerships will be one of the key vectors for competition moving forward. Robinhood was the first major fintech domino to fall – a huge win for the Arbitrum ecosystem – but it won’t be the last. In the end, that will benefit the best on-chain projects (which get integrated into the largest platforms) and the best distribution channels (who can monetize the activity). There is certainly irony in fintech giants capturing the value crypto creates, but that is the unavoidable reality of competition. The race is now on to disrupt or be disrupted.

We are positioned to buy summer softness in alts with short-term risks around inflation, trade policy, or a weak earnings season, but extremely optimistic going into H2 2025. This is shaping up as a very good year for risk assets before potential uncertainty around 2026 midterms For now, the administration is risk-on, monetary policy is loosening, and the biggest companies on Earth are thinking about how to bring a new cohort of users on-chain.