Growing Pains

An industry in an adolescent moment

Market Overview

Markets re-rated higher in Q4 in anticipation of a business-friendly Trump administration, and Q1 was widely thought to be the beginning of a strong year for asset prices. That was not the case, of course, as investors soon found out. In hindsight, the run-up priced in much of the short term upside while incorrectly pricing the downside risks of Trump (in our last report, we called out immigration and tariff policy). The latter is now a major source of global heartburn as everyone knows, and major indices have retraced the entirety of their November moves as a result. Note that BTC is actually up 15% since election day while total crypto market cap is down (as are other risk assets).

With regard to crypto markets, there has been a serious divergence in sentiment. On one hand, retail participants are depressed, having positioned for a bull market with speculative favorites that are now down 60% or more. On the other hand, institutions are as enthusiastic and active as ever given the regulatory shift and expected policy changes. These include new leadership at the SEC, dismissal of virtually every legal action against the industry, and a growing sense of confidence that Stablecoin and Market Structure bills will pass in Q2/Q3 (not to mention a Bitcoin Strategic Reserve). Each of these removes a serious overhang, and it’s easy to be optimistic about the industry’s growth over the long term if you believe in the concept of an upgraded, internet-native financial system. Wall Street certainly does.

In the short term, the picture is less clear. It could take months if not years for some of these things to unfold. Markets move quickly, but institutional allocators do not. We were surprised by the size and scope of the selloff, but with crypto markets now at pre-election levels, there is value to be had in specific sectors given the long-term progress being made.

This cycle could be different

We’ve talked about the trend of dispersion between BTC and other sectors before, and it continued this quarter. Literally nothing outperformed BTC, notably including ETH which is down almost 40% itself as ETH/BTC ratio continues to make new lows.

In every previous crypto “cycle”, BTC initially outperforms, followed by a period of outperformance by lower caps as wealth effect manifests and investors seek more risk. Outside of a very brief period of outperformance in January, there has been no such rotation. We view this as a combination of three factors:

More alt coins than ever before; A function of newly launched projects and egregious token unlock schedules for existing ones. There is simply not enough capital to absorb the ever-increasing supply

More ways to access BTC beta; In the past, altcoins have acted as market beta for investors, but now they can achieve the same risk profile without worrying about asset selection. Namely, equity plays like MSTR and various options and derivatives venues

The marginal buyer of BTC has changed; Institutional buyers who are moving the price of Bitcoin are less likely to be buyers of smaller cap tokens (at least so far)

So is this time really different? That’s a dangerous assumption to make, and we do still expect individual alt coins to outperform majors when risk appetite returns. But we do not expect altcoins to outperform in a highly correlated way as they have in the past. Rather, we expect isolated outperformance based on actual business and revenue growth, not cycle timing and narrative favor.

Positioning for a ‘fundamental’ shift

If you’ve read our letters before you know we are focused on fundamentals. Over the past few years, that has gone from being somewhat contrarian to relatively consensus. That may sound absurd, but it’s not entirely irrational. The market has often rewarded narrative strength over fundamental traction. But that finally seems to be changing. Perhaps it was the over-supply and under-performance of so many buzzy tokens, or perhaps it was the realization that institutions weren’t coming to buy worthless governance tokens in a world where legal value accrual is achievable. We may have been early to the trend, but remain convicted in the handful of projects that have combined winning products with sensible tokenomics. This is great for the space long-term despite the short-term growing pains.

We have reflected this in portfolio construction, cutting positions that relied on narrative momentum, as well as moving 12% of the fund to cash. We now own only 8 non-majors (i.e. not BTC or SOL), all of which have real cash flows and defensible valuations. We expect the investable universe of quality tokens will grow, but at least for now it’s a short list, mostly consisting of financial infrastructure we have covered in the past and that could benefit from a wave of institutional adoption (e.g. MKR, AAVE).

We also remain overweight BTC, which is a bit unimaginative but served us well. Most liquid funds are hard pressed to hold BTC in size given their mandate to outperform it (and as a result, most have not). We certainly suffered a drawdown in Q1, but were somewhat insulated by the relative strength of BTC.

The Trump effect on Solana

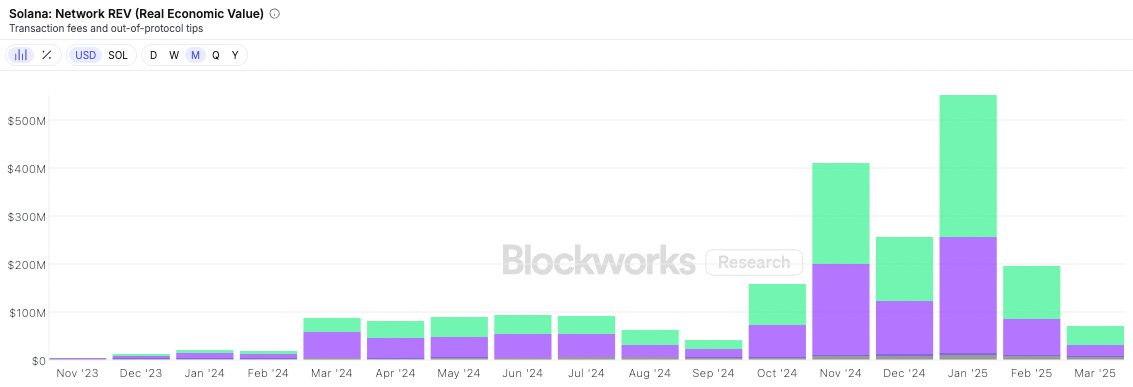

We also remain overweight SOL, though we did reduce the position in February. It was a boom and bust quarter for the network even by crypto standards, marked by a new ATH ($284) in January, followed by a precipitous sell-off in March to ~$130. This tracked network activity, which peaked with the launch of the TRUMP meme coin in January and generated an astounding $550M in fee revenue. That number dropped below $100M in March as meme coin trading activity cratered. This all coincided with an unlock of 11m tokens in early March (the largest to date), which was well understood by the market but poorly timed, as shown by price action.

We have harbored concerns about the sustainability of the meme “economy” for a while and viewed the launch of TRUMP as a worrying sign of froth, even with the astronomical growth that came with it. That said, Solana is still best positioned to win the high performance blockchain market, but needs to find a second act (beyond memecoin trading) to regain traction and continue its ascent. This quarter provided a glimpse of what network economics can look like in a future state, validating the thesis that a high-volume, low-fee model can generate real economic value. Of course, it also invites new questions about where future revenue will come from. Time will tell.

In early January we looked at several Solana apps that were growing revenue quickly and accruing value to token holders, ultimately starting small positions in Raydium (RAY) and Jupiter (JUP) to go along with an existing position in Kamino (KMNO). We quickly exited those positions when it became clear that economic activity was evaporating. Upcoming unlocks make these hard to hold for next several quarters, but could be interesting at lower entries when network activity rebounds.

The unwind of the AI trade and other unattractive ideas

We wrote about AI in Q4, noting it was an obvious megatrend but worrying the current batch of AI bots were mostly “uninspired GPT wrappers masquerading as the next big thing”. The masquerade was short lived, with the broader market downturn effectively wiping out AI sector gains with nearly everything down 90% in Q1. The true long-term believers can probably start looking for comeback stories at these levels, but most of it still looks like vaporware. We closed all of our starter positions here (at a loss).

We are also staying away from the new L1 launches. This includes the cohort that launched in 2024 (e.g. SEI, SUI, APT) that have few apps of note and far too many tokens coming to market. It also includes the new crop of L1s (e.g. BERA, MONAD) which appear to have the same supply issues and lack of differentiation. The L1 relative value trade of past cycles has become a shell game for VCs to pass the bag to over-eager, pattern-matching, retail participants at untenable FDVs. Our view is that existing EVM extensions and Solana will still benefit most from forthcoming development and institutional adoption.

We are following the trend of apps launching their own L1 chains – with the two big recent examples being Ethena and Ondo. From the perspective of the companies, this makes a lot of sense. Like any vertically integrated business, they can control product development and economics. These companies also claim they will be able to onboard more real-world assets and institutions with permissions and customization, which is obviously a good thing. And there is likely a valuation premium that comes along with owning the network, even if it’s eroding.

From the perspective of a user, it’s quite frustrating to bridge between chains to access different apps and fragmented liquidity. The companies pursuing these chains will tell you that future development will abstract away most of the current pain points, but we are skeptical that a world with more chains and fewer standards is the most user-friendly approach.

From the perspective of the industry, each product existing inside a walled garden starts to look suspiciously like the existing internet we set out to change. Note that “app-chains” seem inevitable for all the same business reasons, but exist within the context of existing architecture and interoperability rather than trying to create new ones. We are open-minded to anything that improves the ultimate user experience, but would rather see chains optimize for speed and security than self-interest.

What we’re still excited about

It’s hard to know what the next few months will look like, but we are always looking for good tokens at good prices. A few that we’re currently considering:

Hyperliquid (HYPE)

Like many others, we were sidelined as it ran from $5B to $30B FDV the week it launched. We have always believed there would be a niche for a less-regulated alternative to the centralized exchange behemoths, and Hyperliquid now boasts an extraordinary lead over its competition. Market share in this sector is notoriously fickle, but the combination of goodwill engendered by a generous airdrop and relentless product execution have set Hyperliquid apart.

At a sub-$10B adjusted market cap ($12B FDV, 40% of which is set aside for future community grants) and $300M+ in revenue, Hyperliquid’s derivatives exchange looks fairly priced considering their growth, as well as the upcoming launch of their spot exchange and L1 – dubbed HyperEVM. We are somewhat skeptical of the L1 play, but the existing userbase is certainly an interesting distribution advantage.

The concern with buying $HYPE here is that a big chunk of supply is still coming to market in the form of a second airdrop and team/foundation unlocks. That is somewhat offset by the fact that there are no investors (bootstrapped by the founder), as well as an aggressive buyback program instituted in Q1. Syncracy has an excellent report for further context.

Jito (JTO)

Multicoin released a comprehensive valuation report on Jito ($JTO), which is now a critical component of Solana infrastructure. The easiest way to think about Jito is a fast lane for transaction processing, on which they take a small fee (currently ~30 bps). The question of valuation comes down to the moat around this feature as Solana matures. We assume that demand for priority processing will always exist on Solana, and that the value of Solana blockspace will increase over time.

We are also optimistic that Jito will maintain a competitive advantage on the product side even though they will become an obvious target as opportunity size gets bigger and Jito experiments with value capture. But we are less convinced that Jito can own a larger and larger share of value accrual as the network grows – Jito is worth ~2% of Solana network now and processes 50+% of fee revenue – especially with the possibility of protocol-level changes to SOL issuance/economics.

Celestia (TIA)

As Solana has grown, narrative has shifted away from the modular blockchain approach (i.e. Ethereum-centric) to a more monolithic one. However, as meme coin mania subsides and EVM infrastructure improves, we foresee a renaissance of sorts for modularity (after all, Solana has rollups too).

Ethereum’s core services are asset storage, execution, and data availability. Storage will always happen on Ethereum mainnet and execution is increasingly happening on L2s, but the market for data availability is up for grabs. As applications outgrow mainnet infrastructure and launch their own appchains, they will have to purchase data availability from somewhere.

Celestia has the best DA product in the market today. They innovated with the concept of DA sampling (essentially, users can verify the chain without downloading all of its data), and currently offer a faster product at a lower price than Ethereum, their primary competitor.

The bear case for TIA is that valuation (~$3B) is too high given they are effectively pre-revenue and their pricing power is unproven. It’s also still on the wrong side of its unlock schedule with 34% of in-profit investors tokens coming to market. But If you believe in the Ethereum ecosystem but not in ETH the asset (as we do), and you believe that Celestia will be critical infrastructure in that ecosystem, TIA looks like an interesting way to express that view.

Looking ahead

As the title suggests, crypto is in its awkward teenager phase. Depending on your perspective, that can feel like the precipice of opportunity or a period of despair. We find ourselves alternating between the two at times. Some things are taking longer than expected – such as non-financial use cases – while others are happening much faster – such as stablecoin issuance (up another 10% this quarter) and support from the American government.

Eventually, the industry’s self-doubt will yield to a more mature understanding of itself, at which point the focus can finally shift to the reality of its usefulness rather than speculation on its potential. One thing that remains obvious to us is the opportunity to update the global financial system, and we will continue to invest in that outcome.

As always, reach out if you have thoughts or questions about anything we’ve written.